Harry (49) and Sally (46) are married with two children who are currently in 4th and 6th year in secondary school. Harry is a solicitor who established his own legal firm in 2010. He currently has 6 employees including Sally who works on a part time basis. Sally is happy to increase her hours

They have managed to accrue a solid asset base over the past ten years. In addition, Harry is expecting an inheritance from his parent’s estate in the region of €480,000 once probate is finalised next year. They are both currently in good health and have no adverse medical family history.

Harry is concerned that his family’s wellbeing is dependent on his ability to drive the profitability of the firm. He particularly want to know if they have enough to maintain their current lifestyle in the event either of them dying suddenly or being unable to work through sickness and disability.

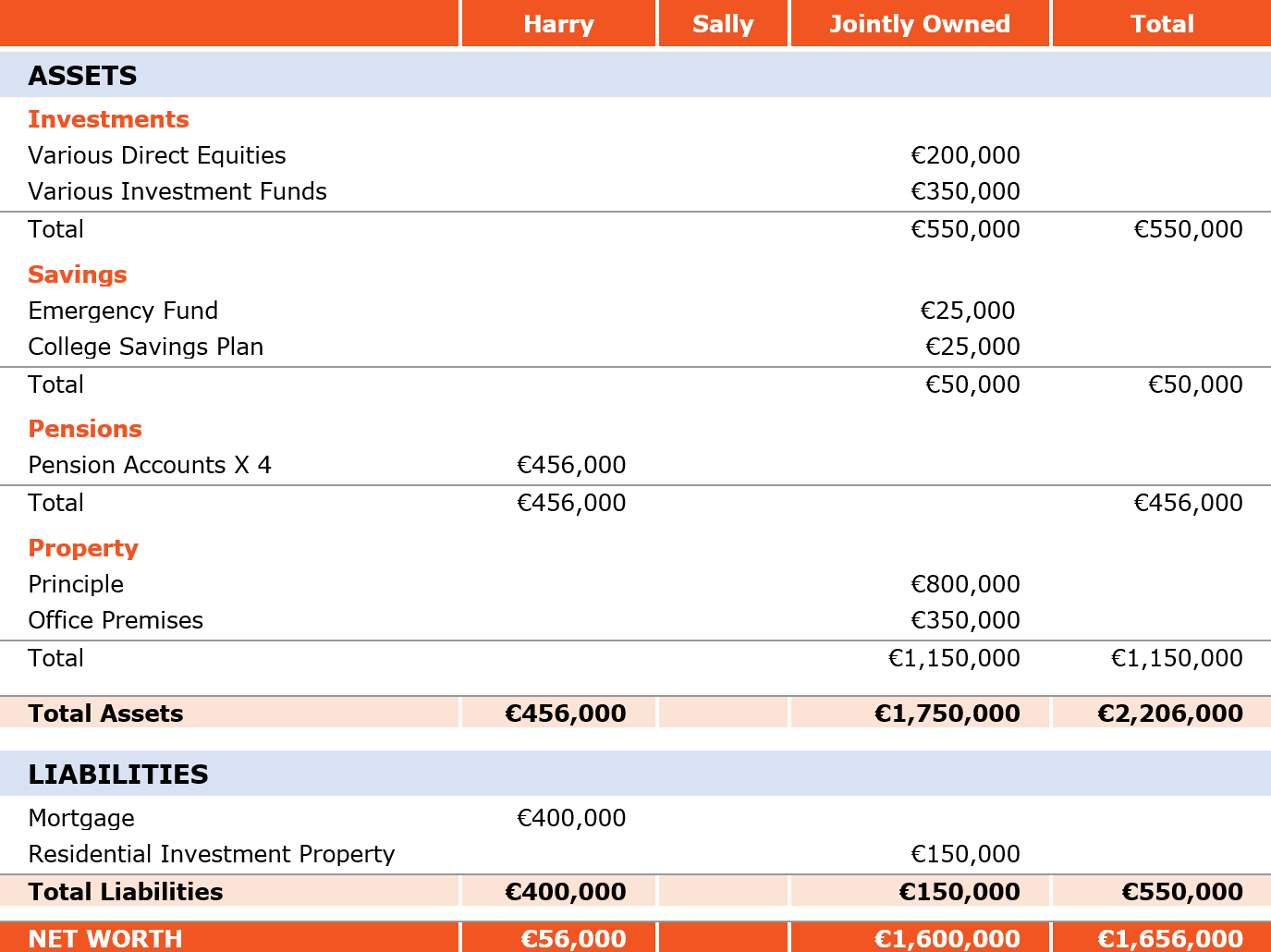

We have outlined their summary balance sheet and income versus expenditure below.

BALANCE SHEET

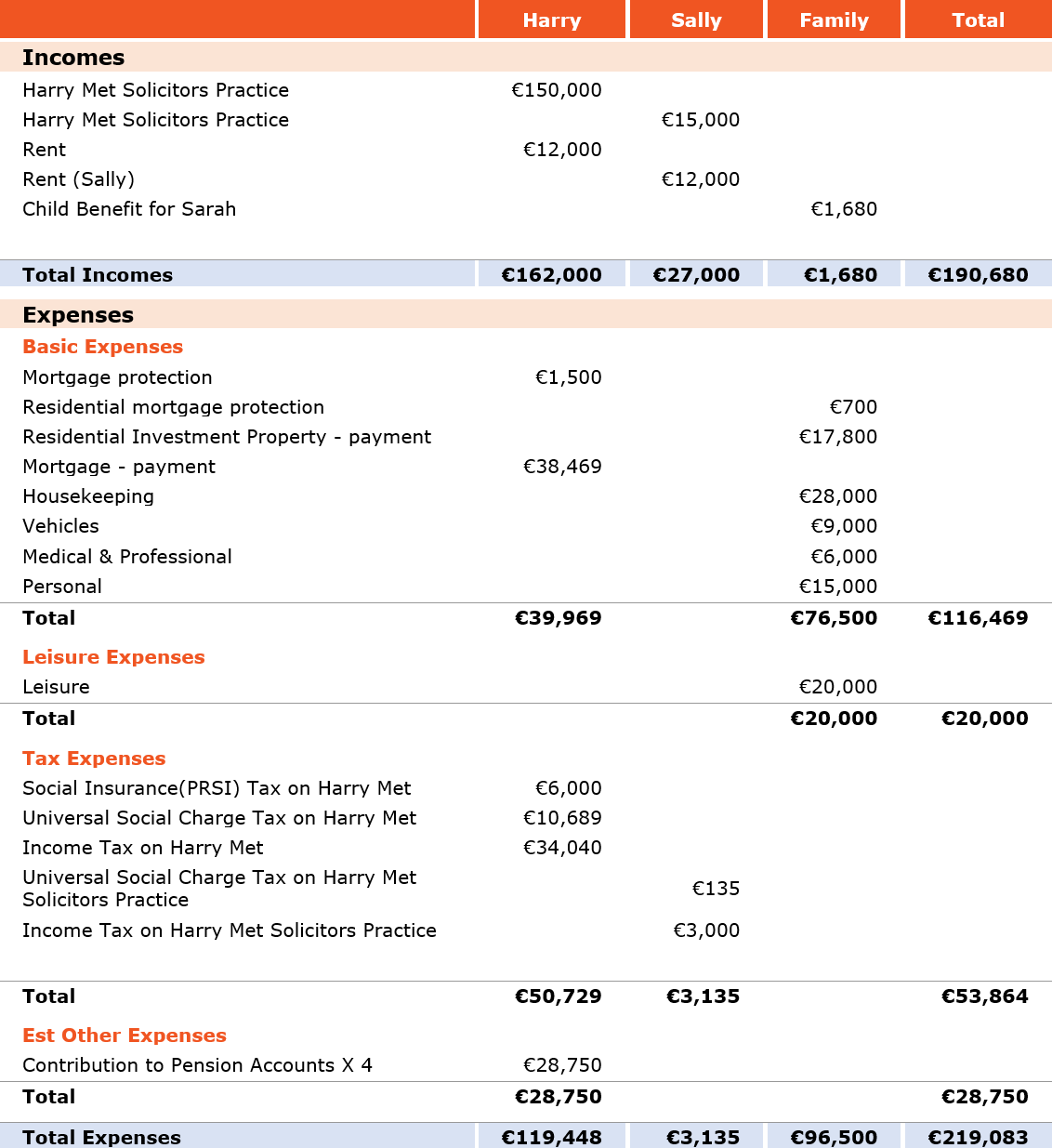

INCOME VS. EXPENDITURE

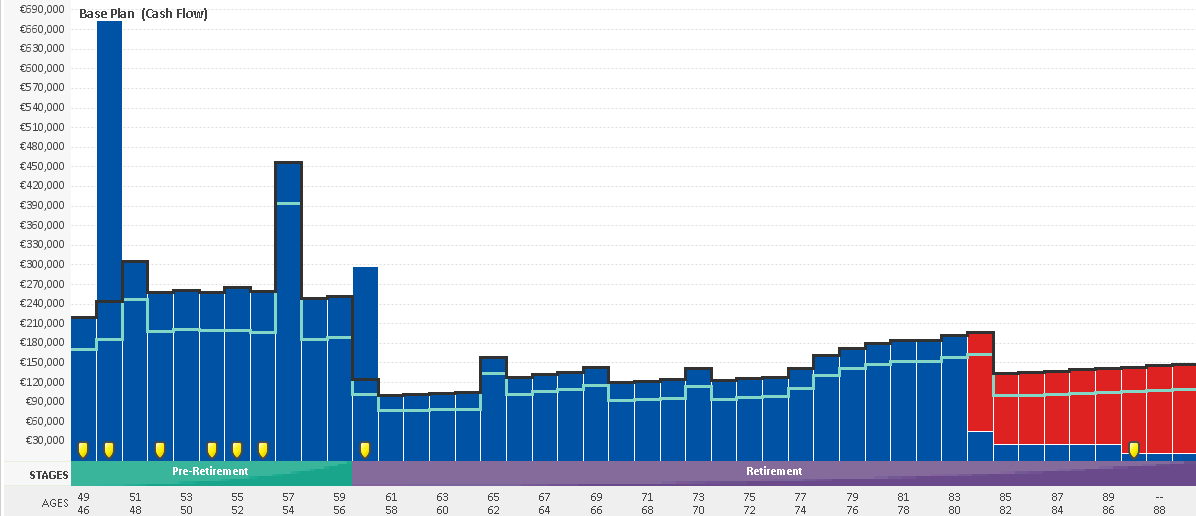

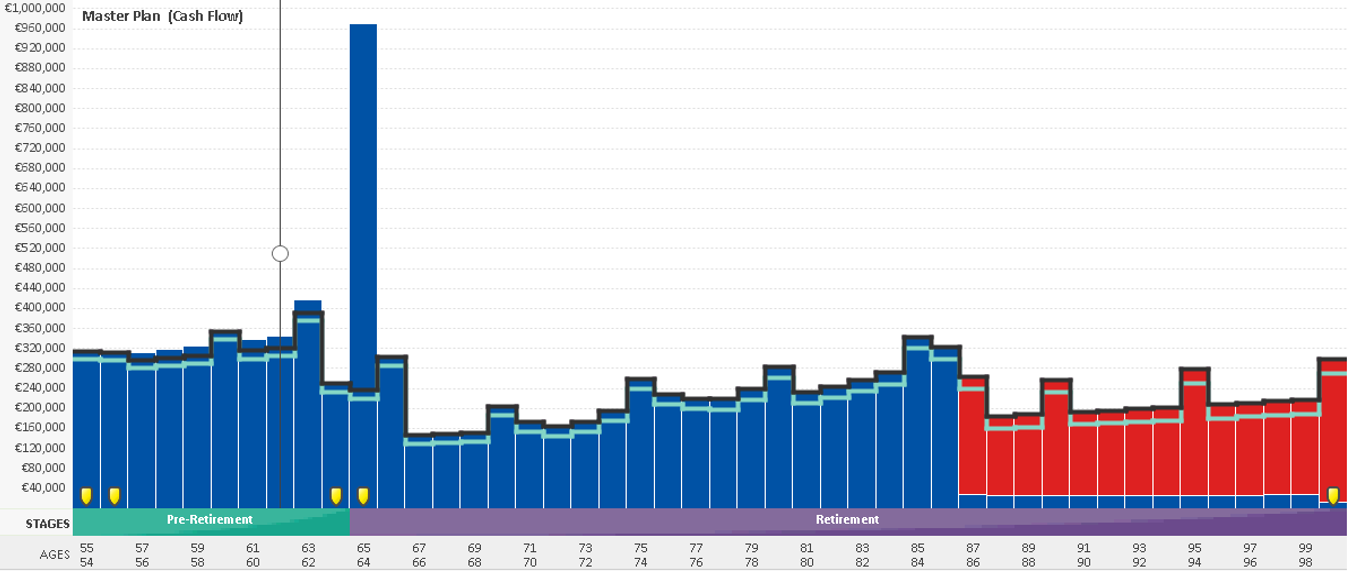

Current Cash Flow Position

Observations

The blue above denotes positive cash flow whilst the red is negative. The black line in the chart above denotes cost of living and any blue above the black line indicates surplus income. Based on the client’s current position, and assuming Harry retires at age 60, they will run out of liquid cash when Harry reaches age 84. We note that that current expenditures exceed current income.

As Harry is self-employed, all of his net relevant earnings after expenses are subject to income tax. To improve tax efficiencies, he may want to consider at a minimum increasing Sally’s remuneration to avail of the full standard income tax band which can be duly financed by a reduction in his own relevant earnings which are taxed at the higher marginal rate.

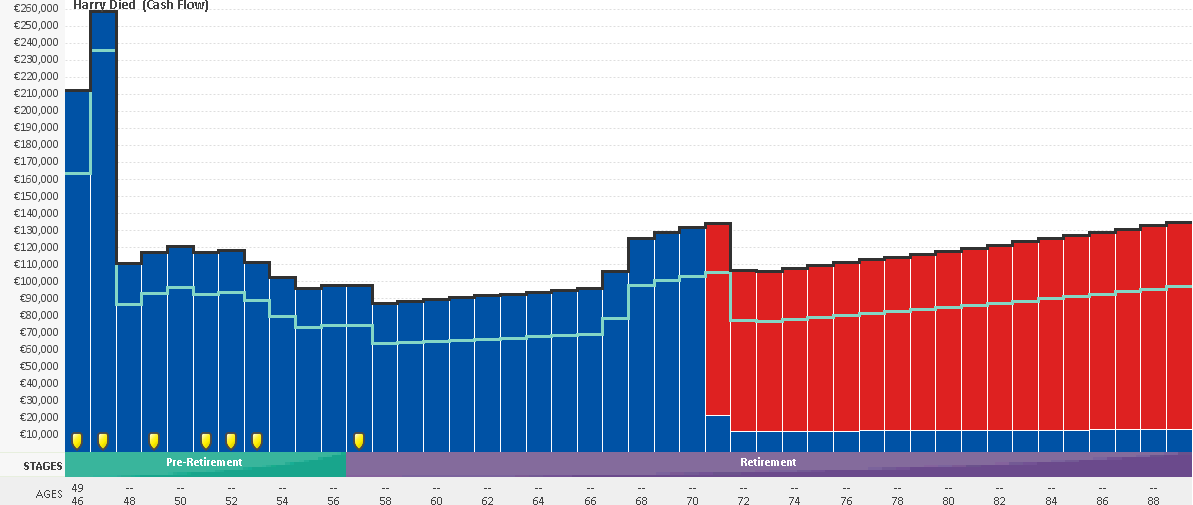

The following charts illustrates Harry and Sally’s current position in the event of either of them dying or being unable to work:

We have outlined their summary balance sheet and income versus expenditure below.

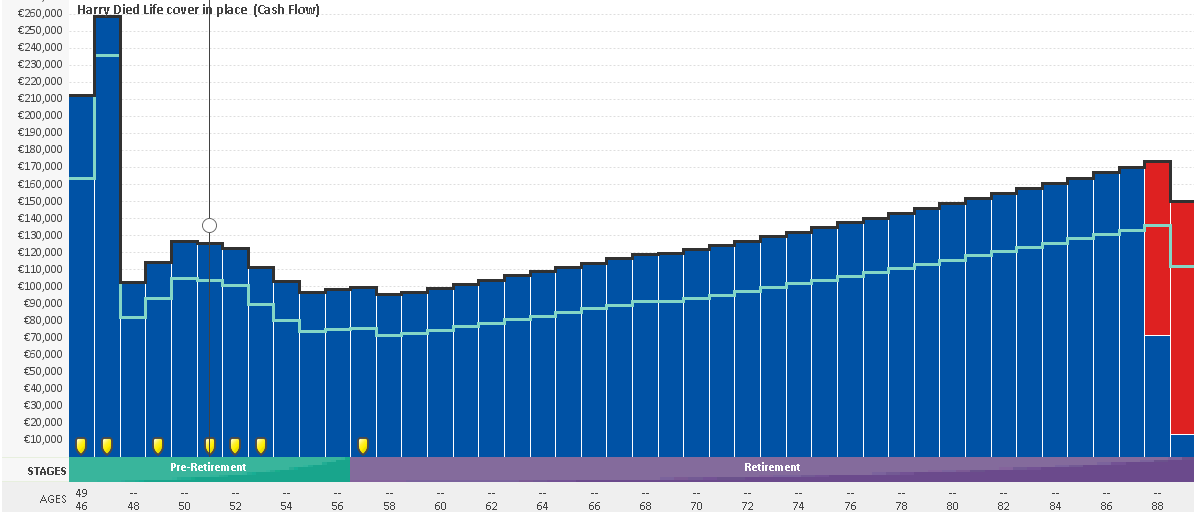

What if Harry died next year

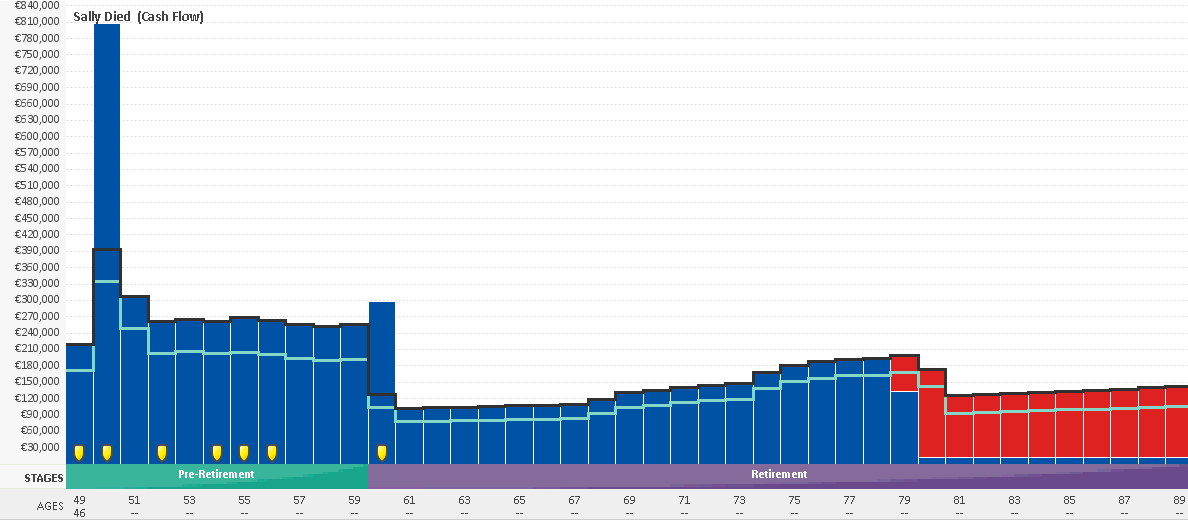

What if Sally died next year

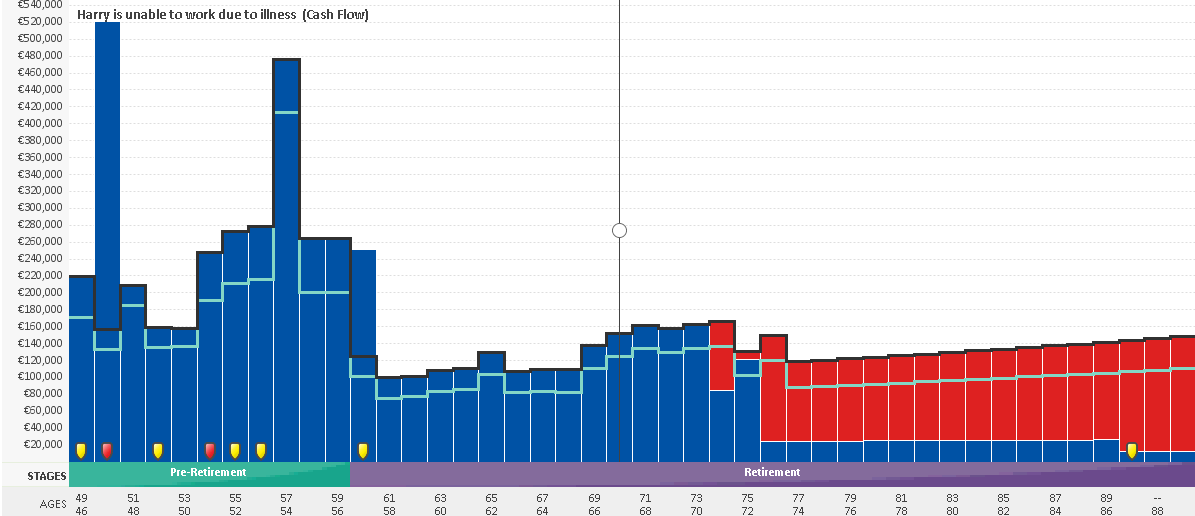

What if Harry was unable to work due to illness

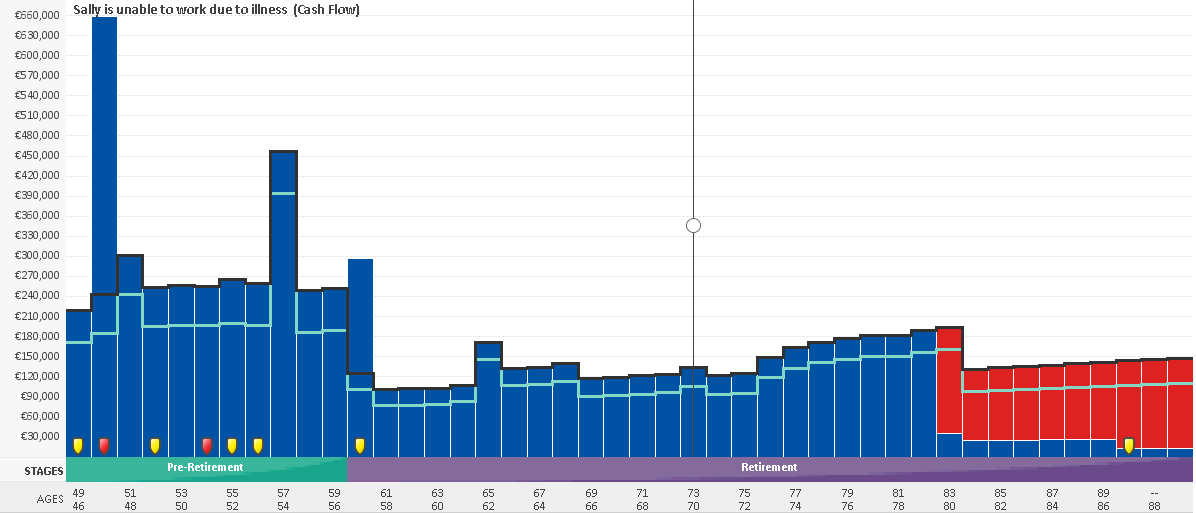

What if Sally was unable to work due to illness

Our initial findings are as follows:

As a priority, a more robust protection strategy should be implemented. With ongoing planning and monitoring of the existing assets incorporating a portfolio approach in line with their risk profile and objectives, the current cash flow scenario can be improved.

Harry and Sally cash flows are negatively impacted in the event of either person dying early or unable to return to work due to illness. Harry is self-employed and is therefore not eligible to receive state disability.

We recommend ongoing analysis of expenditures to ensure their accuracy and to achieve any efficiencies going forward.

We have outlined their summary balance sheet and income versus expenditure below.

Strategy

Based on the current income figures, we recommended the following:

They effect a joint Life and accelerated specified illness mortgage protection policy with a sum assured sufficient to fully discharge all debt in the event of either of them dying or being diagnosed with a qualifying specified illness during the term of the policy.

They cancel their existing mortgage protection policies once the new policy issues.

To increase the level of personal life cover:

Harry’s to provide a death in service benefit for Sally under the solicitors practice equating to four times her salary, e.g. €60,000 based on current salary.

Harry to effect a pension term life assurance for a sum assured of €400,000 whereby he can claim marginal rate tax relief on the premiums.

Harry effects an income protection policy for the maximum permitted equating to 75% of earnings, e.g. €112,500 based on a 75% of €150,000. (As Harry is self-employed, he does not currently qualify for State Disability).

Implement an investment strategy for both their pension and investment assets targeting a long term rate of return of 4.5% net of fees.

All savings are assumed to be held in cash at a long term rate of 1.5%

Monitor the plan on an ongoing basis to ensure it remains on track.

What if Harry dies next year with increased life cover

What if Sally dies next year with increased life cover

What if Harry was unable to work due to illness

What if Sally was unable to work due to illness

The above charts do not include the option to liquidate their investment property at a future point.

Wealth Alliance Limited is registered in Ireland.

Wealth Alliance Ltd is regulated by the Central Bank of Ireland C120055. Directors: Brenda Rogan & Jane McAleese.